The document your CCO has always needed. Now generated automatically.

No other compliance tool in this market generates a formal, exportable Compliance Memo — a structured narrative document that records what was reviewed, which regulations applied, what issues were found and resolved, and why the final content meets the standard. Marcovio does.

★★★★★ The artifact compliance officers actually file when regulators come calling

The formal compliance record, auto-generated when you're done.

When a marketer declares their content complete inside Marcovio, the platform automatically generates a Compliance Memo — a structured, formal document that records what was reviewed, which regulations applied, what issues were found and resolved, and why the final content meets the standard.

It's not a dashboard report. It's not a pass/fail badge. It's a professional narrative document — the kind you attach to a regulatory examination response, file in your compliance records, or send to a client as proof of diligent review.

Every section a compliance officer needs. Nothing they don't.

| Asset Reviewed | Description of the content, asset type, date, and campaign context |

| Applicable Regulations | The specific rules checked — e.g., SEC Rule 206(4)-1, FINRA Rule 2210, FTC guidelines |

| Compliance Analysis | A plain-English explanation of how the content meets each applicable rule |

| Review History | What was flagged, what was changed, and by whom — the full iterative trail |

| Compliance Determination | The final compliance status with supporting rationale |

One document. Three audiences who need it.

💼

Compliance Officer / CCO

The Memo gives compliance officers a defensible record that proves the firm has a documented, systematic review process — it is what they attach to regulatory correspondence.

💼

Marketing Leader / VP Marketing

For marketing leaders, the Memo closes the loop. Content doesn't just get an approval — it gets a record.

💼

Agency Creative / Copywriter

Agencies use the Memo to demonstrate compliance diligence to clients. On Enterprise plans, memos are generated under the client's configuration.

Regulations Marcovio Evaluates

Marcovio's AI analyzes your marketing content against 38 regulations from SEC, FINRA, MSRB, and other regulatory bodies — ensuring comprehensive compliance coverage across all financial services marketing channels.

The Marketing Rule

Rule 206(4)-1

The foundational rule governing all advertising and marketing by investment advisers, replacing the prior advertising rule in November 2022. Prohibits seven categories of misleading content and regulates the use of testimonials, endorsements, and third-party ratings under strict disclosure conditions.

Books and Records — Advertising Recordkeeping

Rule 204-2

Requires registered investment advisers to maintain copies of all advertisements and promotional materials, including drafts and revisions. Materials must be retained for five years and accessible to SEC examiners on request.

Compliance Programs

Rule 206(4)-7

Requires registered investment advisers to maintain a written compliance program covering marketing and advertising, designate a Chief Compliance Officer, and conduct annual reviews of marketing policies.

Investment Company Advertising

Rules 156 and 482

Governs advertising and sales literature for registered investment companies. Rule 156 prohibits misleading statements about performance, risks, or fees; Rule 482 establishes requirements for omitting prospectus advertising, including what information can be included when marketing fund products without full prospectus disclosure.

Regulation S-P — Privacy of Consumer Financial Information

Regulation S-P

Requires privacy notices when collecting and using customer data for marketing, restricts sharing of customer nonpublic personal information with affiliates and third parties for marketing purposes, and mandates that opt-out rights be disclosed and honored.

Regulation Best Interest — Marketing Implications

Regulation Best Interest (Reg BI)

While primarily an investment advice rule, Reg BI has marketing implications: broker-dealers cannot advertise themselves as advisors in ways that imply a fiduciary relationship they do not hold, and must disclose material conflicts of interest. Form CRS is treated as a marketing communication and must be written in plain English.

AI-Specific Enforcement Actions (2024)

N/A — Enforcement Actions

In March 2024, the SEC charged two advisory firms specifically for making false claims about their use of AI in marketing materials. Advisers cannot claim to use AI systems in managing client assets if they do not, and AI-generated marketing content is subject to the same accuracy and disclosure standards as human-written content.

FINRA Rule 2210 — Communications with the Public

FINRA Rule 2210

The central rule governing all broker-dealer marketing. Divides communications into three categories — correspondence, retail communications, and institutional communications — each with different approval and filing requirements. All communications must be fair, balanced, and not misleading.

FINRA Rule 2210 — Social Media Guidance

FINRA Rule 2210 / Regulatory Notice 17-18

Provides specific guidance on how FINRA Rule 2210 applies to social media. Differentiates between static content (websites, profile pages — treated as retail communications) and interactive content (real-time posts, comments — treated as correspondence). Personal accounts used for business purposes are covered.

FINRA Rule 2210 — Influencer and Third-Party Marketing

FINRA Rule 2210

Governs how FINRA Rule 2210 applies to influencer and third-party marketing arrangements. Firms are responsible for content created by paid promoters, and compensation arrangements with influencers must be disclosed. All influencer content must comply with fair, balanced, and non-misleading standards.

FINRA Rule 2241 — Research Analyst Conflicts

FINRA Rule 2241

Governs the use of investment research in marketing. Research reports used in marketing must disclose analyst compensation and conflicts, and marketing materials cannot misrepresent or cherry-pick analyst conclusions.

FINRA Recordkeeping Rules

FINRA Rules 4511 and 4512

Requires FINRA member firms to retain all marketing and advertising materials for three years (six years for certain categories). Electronic communications, including social media, must be archived and communications used in customer interactions must be retrievable for examination.

MSRB Rule G-21 — Advertising by Municipal Securities Dealers

MSRB Rule G-21

Prohibits false or misleading advertisements relating to municipal securities, and requires specific disclosures for municipal fund securities including 529 plans. Explicitly covers all digital and social media as of a 2019 amendment, and requires principal approval before publication.

MSRB Rule G-40 — Advertising by Municipal Advisors

MSRB Rule G-40

Applies the same fair-and-balanced content standards to municipal advisors as Rule G-21 applies to dealers. Testimonials must be disclosed with compensation arrangements, all advertisements require supervisor approval, and social media static content is explicitly treated as advertising.

MSRB Rule G-17 — Fair Dealing

MSRB Rule G-17

Broad prohibition on deceptive, dishonest, or unfair practices in marketing. Often cited in conjunction with G-21 advertising violations.

NFA Compliance Rule 2-29 — Communications with the Public

NFA Compliance Rule 2-29

Governs all promotional materials for futures and commodities firms. All promotional materials must be fair, balanced, and not misleading. Strict requirements apply to performance advertising, hypothetical and simulated performance results, and documentation of all promotional materials.

CFTC Regulation 4.41 — Promotional Material

CFTC Regulation 4.41

Federal-level counterpart to NFA Rule 2-29. Requires specific disclosures for past performance, hypothetical performance, and risk in all promotional materials, including the CFTC-mandated risk disclosure statement.

UDAAP — Unfair, Deceptive, or Abusive Acts or Practices

Dodd-Frank Act Section 1031

The broadest and most flexible consumer protection standard in financial services. Prohibits marketing that is unfair, deceptive, or abusive. Financial firms can be held liable for UDAAP violations committed by their marketing agencies, affiliates, or third-party lead generators.

MAP Rule — Mortgage Acts and Practices Advertising

Regulation N

Specifically prohibits unfair or deceptive advertising in mortgage marketing. Prohibits misrepresentations about interest rates, APR, payment amounts, fees, loan terms, prepayment penalties, and the consumer's ability to obtain refinancing. Also prohibits deceptive use of government affiliation or endorsement imagery.

Truth in Savings Act — Regulation DD

Regulation DD

Requires deposit account advertisements to use specific standardized terms and make clear disclosures about bonuses, fees, and APY. Prohibits advertising accounts as 'free' if conditions or fees would make a typical consumer's account subject to fees.

Truth in Lending Act — Regulation Z Advertising

Regulation Z

Governs advertising of consumer credit products. The 'trigger terms' rule requires full APR disclosure whenever any specific credit term is mentioned. Specific rules apply to credit cards, teaser rates, and mortgage advertising.

Fair Housing Act and ECOA — Marketing Implications

Fair Housing Act / ECOA

Prohibits using race, color, religion, national origin, sex, disability, or familial status as factors in targeting or excluding advertising audiences. Digital 'redlining' violations can occur through exclusionary geographic or demographic targeting. Marketing agencies can be held liable for discriminatory targeting practices.

FTC Act Section 5 — Unfair or Deceptive Acts or Practices

FTC Act Section 5

The foundational federal advertising law. Prohibits any advertising that is deceptive or unfair, and requires advertisers to have a 'reasonable basis' for any objective claim before publication. Covers all media.

FTC Endorsement Guides

16 CFR Part 255

Requires that all material connections between an advertiser and an endorser be clearly and conspicuously disclosed. Revised in July 2023 with explicit definitions of 'clear and conspicuous,' expanded coverage to virtual influencers and AI-generated avatars, and explicit liability for agencies and intermediaries.

FTC AI Guidance — Marketing Claims About AI

FTC Guidance and Enforcement Actions, 2023–2024

FTC guidance and enforcement actions establishing that marketing claims about AI capabilities must be accurate and substantiated. 'AI washing' — claiming to use AI when you do not — is a deceptive practice. The FTC is developing further rulemaking on AI in advertising.

CAN-SPAM Act — Email Marketing

CAN-SPAM Act

Sets requirements for all commercial email, including accurate sender identification, truthful subject lines, a physical mailing address, and a functioning opt-out mechanism. Opt-out requests must be honored within 10 business days. Financial content in email remains subject to all other applicable regulations.

TCPA — Telephone Consumer Protection Act

TCPA

Requires prior express written consent before sending automated calls, pre-recorded messages, or text messages for marketing purposes. Do-Not-Call list compliance is mandatory. One of the most actively litigated consumer protection laws, with significant class action exposure.

Gramm-Leach-Bliley Act — Privacy in Marketing

Gramm-Leach-Bliley Act (GLBA)

Requires financial institutions to provide clear privacy notices explaining what data is collected and how it's used. Consumers must have an opportunity to opt out of sharing with non-affiliated third-party marketers. Privacy notices must be available on websites and renewed annually.

FDIC Advertising Rules

12 CFR 328

FDIC-insured banks must include the official FDIC membership statement in all advertising. The FDIC sign and statement cannot be used in advertising for non-deposit products such as mutual funds, annuities, or stocks, and cannot be used in ways that imply non-deposit products are FDIC-insured.

Non-Deposit Investment Product (NDIP) Rules

NDIP Rules (Interagency Guidance)

All marketing for investment products sold through a bank must clearly state the product is 'Not FDIC-insured,' 'Not a deposit,' 'Not guaranteed by the bank,' and 'May lose value.' These disclosures must be prominent and cannot be buried in fine print.

Community Reinvestment Act (CRA) — Marketing Implications

Community Reinvestment Act (CRA)

Banks cannot market services in ways that exclude low- and moderate-income (LMI) communities. Geographic targeting of marketing must not systematically exclude LMI areas. Marketing channel selection can be examined for CRA compliance.

CCPA / CPRA — California Consumer Privacy Act

CCPA / CPRA

Grants California consumers the right to opt out of the sale or sharing of their personal information, which includes targeted advertising and data sharing with ad tech platforms. Requires a 'Do Not Sell or Share My Personal Information' link on websites. CPRA (2023) added the right to opt out of sharing for cross-context behavioral advertising.

Other State Privacy Laws

VCDPA, CPA, CTDPA, TDPSA, and others

Virginia (VCDPA), Colorado (CPA), Connecticut (CTDPA), Texas (TDPSA), and other states have enacted privacy laws following a similar model to CCPA. Firms with national marketing campaigns need a framework that satisfies all applicable state laws. Key marketing implications mirror CCPA: opt-out rights, data transparency, and limitations on behavioral advertising.

GDPR — General Data Protection Regulation

GDPR

Requires a lawful basis for processing personal data for marketing, with consent being the typical basis for direct marketing. Consent must be freely given, specific, informed, and unambiguous. Fines can reach €20 million or 4% of global annual revenue, whichever is higher.

SEC and FINRA Social Media Guidance

N/A — Combined Regulatory Guidance

Firms are responsible for all content published through any channel, including personal social media accounts used for business. Static posts are treated as retail communications requiring principal approval; interactive content may be treated as correspondence but remains subject to supervision. All business-related social media must be archived.

AI-Generated Content — Regulatory Considerations

N/A — Multi-Regulator Guidance

AI-generated advertising is held to the same accuracy and disclosure standards as human-created content. No AI-specific marketing rules have been finalized yet, but the FTC, SEC, and CFPB have all signaled increased scrutiny. Key risk areas include unsubstantiated performance claims, hallucinated regulatory citations, disclosure omissions, and AI washing.

Influencer and Third-Party Marketing — Combined Regulatory View

N/A — Multi-Regulator Guidance

When a financial services firm engages influencers, affiliates, lead generators, or any third-party marketer, multiple regulations apply simultaneously across the FTC, FINRA, SEC, MSRB, and CFPB. Firms bear responsibility for third-party content and compensation must be disclosed across all regulatory frameworks.

Recordkeeping and Documentation Standards

N/A — Multi-Regulator Standards

Across all applicable regulations, financial services firms must meet documentation standards for pre-publication review, archiving, and retention of all marketing materials. In regulatory examinations, examiners will ask to see copies of all marketing materials, records of approval, regulatory basis for claims, third-party relationship documentation, and consumer complaint records.

Here's what a Marcovio Compliance Memo looks like.

COMPLIANCE MEMO

Generated by Marcovio · marcovio.com

Date:

February 18, 2026

Prepared for:

Coastal Wealth Advisors — Marketing Team

Asset Type:

Social Media Post (LinkedIn)

SECTION 1 — ASSET REVIEWED

"Coastal Wealth Advisors has helped clients achieve consistent above-market returns for over 15 years. Our personalized approach to portfolio management has outperformed the S&P 500 in 12 of the last 15 years. Schedule a complimentary consultation today."

SECTION 2 — APPLICABLE REGULATIONS

- SEC Rule 206(4)-1 — Investment Adviser Marketing Rule

- FINRA Rule 2210 — Content Standards

- FTC Advertising Guidelines — Substantiation requirements

SECTION 3 — COMPLIANCE ANALYSIS

Issue identified and resolved: Unsubstantiated performance claim. The original draft contained the claim "consistent above-market returns" and "outperformed the S&P 500 in 12 of the last 15 years." Under SEC Rule 206(4)-1, performance advertising must include required disclosures or be removed.

SECTION 4 — REVIEW HISTORY

| Draft v1 | Feb 17, 2026 | Initial submission | J. Torres |

| Draft v2 | Feb 18, 2026 | Removed performance claims per AI flag | J. Torres |

| Final | Feb 18, 2026 | Compliance review complete | Marcovio AI |

SECTION 5 — COMPLIANCE DETERMINATION

Status: ✓ COMPLIANT

This Compliance Memo was generated by Marcovio AI on February 18, 2026. It documents the AI-assisted review process and does not constitute legal advice.

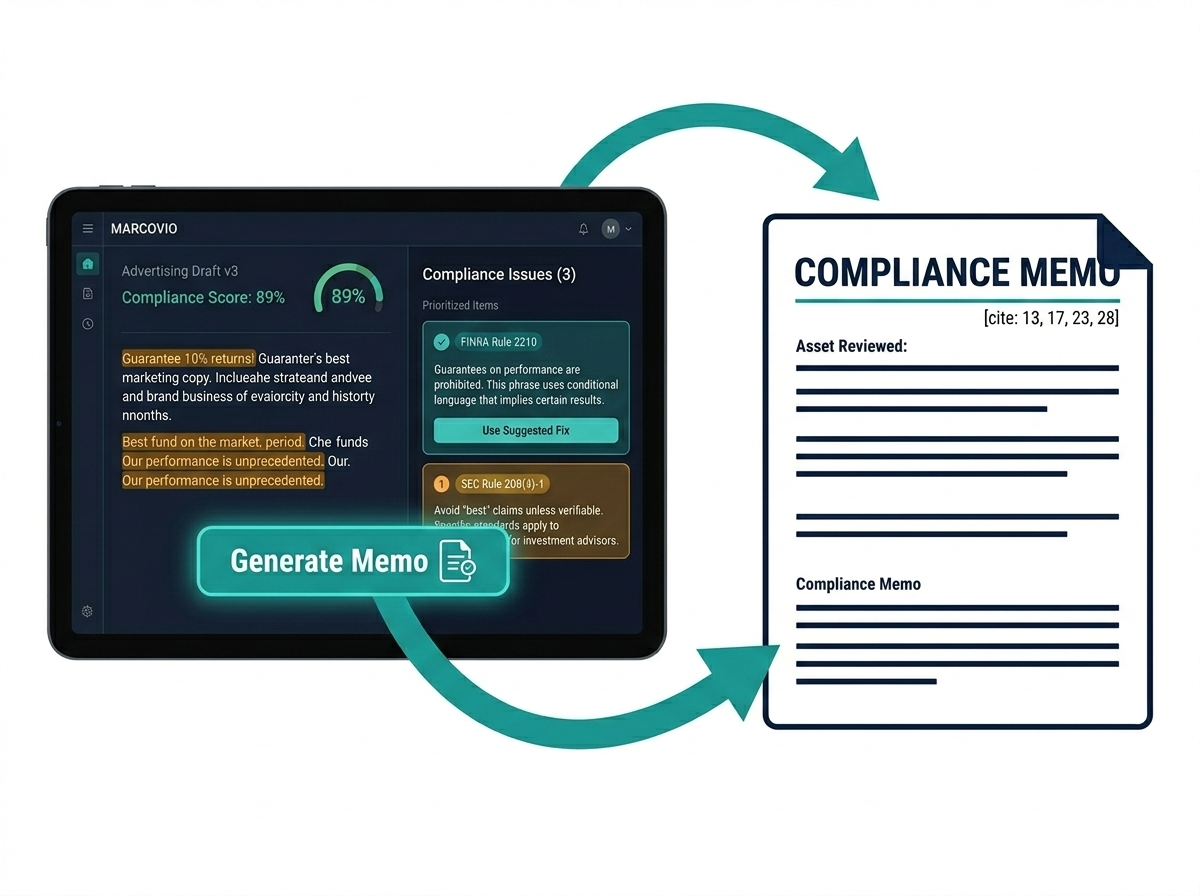

From review to memo in one click.

01 — Review your content

Submit your draft marketing asset. Marcovio's AI analyzes it against rules and suggests alternatives.

02 — Declare it complete

Click "Mark as Complete" to trigger memo generation.

03 — Your memo is ready

Download or export PDF/Word; send to your CCO or archive.

We looked at every compliance tool on the market. Not one of them generates this document.

Every other platform produces dashboards or logs — Marcovio produces the exportable Compliance Memo compliance teams can file.

| Formal exportable compliance memo | ✗ No tool | ✓ Only Marcovio |

| Specific regulation citations in narrative form | ✗ No tool | ✓ Only Marcovio |

| Document suitable to attach to regulatory response | ✗ No tool | ✓ Only Marcovio |

The Compliance Memo is available on every paid plan.

| Compliance Memos / month | 1 (Basic) | 10 | 40 | 150 | Unlimited |

| PDF / Word export | — | ✓ | ✓ | ✓ | ✓ |

| Custom memo format & sections | — | — | — | ✓ | ✓ |

| White-labeled memo (agency branding) | — | — | — | — | ✓ |

Frequently Asked Questions

No. The Compliance Memo is a documentation artifact generated by AI that records the compliance review process. It is not legal advice.

On Business and Enterprise plans, you can configure the memo's sections, disclosure language, and formatting.

Every plan includes pre-loaded rule sets for SEC, FINRA, FTC, and HIPAA. The AI references the specific rule provisions relevant to the content.

Regulators evaluate documentation based on substance and consistency. A clear memo supports a defensible program, but it is not legal advice.

An audit trail is operational event data. A Compliance Memo is a narrative document explaining why content is compliant.

Your first Compliance Memo is one review away.

See how Marcovio fits your firm's review workflow in a live demo.